A research note from Goldman Sachs furthering their theme that they expect more US dollar appreciation.

I post bank research like this quite often, we all do here at ForexLive. You may agree or disagree with the views expressed by the bank quoted (in this case Goldman Sachs looking for further USD strength). We don't post this stuff for ForexLive traders to blindly follow along, nor to blindly 'fade' it, that's not the point at all. Evaluate it yourself, form your own views.

Another way to use these notes is as a learning resource.

For example, in this note (I'll put the full text up down below .... I'm gettin' there!) I really like this:

"negotiations between Greece and its creditors means the market has low visibility, unable to trade beyond the immediate headlines"

This is a very, very good point. Headlines surrounding the Greek negotiations have been catalysts for market moves, and this has intensified in recent weeks. Headlines re Greece have not been the only catalysts, of course, we've had swings in response to 'risking' and 'derisking' as Chinese stockmarkets have done the roller-coaster ride thing these past weeks also (the AUD, for example, has been responsive to Chinese moves during trading hours on China stocks markets). And the usual round of central bank speak and economic data points, and so on.

The point it, this is an unusually headline-driven market, its very sensitive to news. When markets are in this heightened state of responsiveness to headlines, limit orders on the orderboards dissipate. They don't all disappear, but they generally diminish in size and there are less of them. Once a move starts (on a headline like"Greece is all good!", or "Its all over for Greece!", for example) it can move quickly through levels that might otherwise have had stiffer support or resistance.

The uncertainty around the negotiations between Greece and its

creditors means the market has low visibility, unable to trade beyond

the immediate headlines, notes Goldman Sachs.

"In this situation, the market seems persistently to err on the side of

optimism, discounting negative developments to focus on the prospects

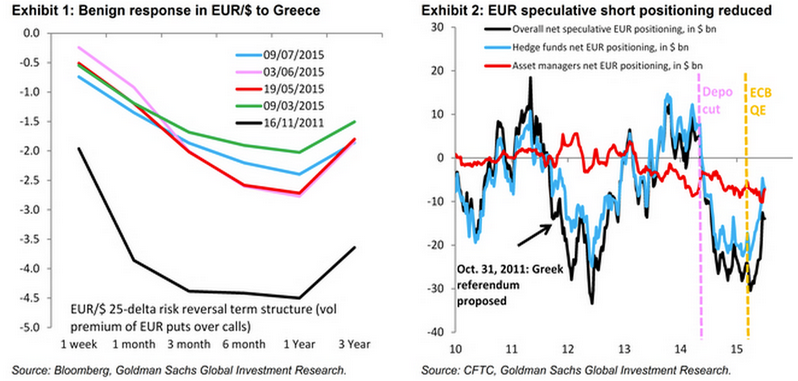

for a positive resolution. This has been reflected in the modest

reaction in peripheral spreads, equities and the EUR," GS adds.

"After all, EUR/$ reflects the market's expected range of outcomes and the probabilities it assigns to these.

Our read is that the market continues to expect a last-minute deal, a

view that is understandable given that this has been the outcome in

every previous confrontation over Greece. Most simply, this should be

apparent from the bounce in EUR/$ on this week's headlines that some

kind of accommodation could be found by the weekend," GS notes.

"In short, even as 'Grexit' risk mounts and is arguably more elevated than ever before, the market does not believe it. We continue to see further escalation as a catalyst for EUR/$ to move near parity,

given that ECB QE, which buffers European stock and bond markets, means

that EUR/$ downside is the only reasonable hedge for investors, unlike

back in 2011/12," GS argues.

"Our broad G10 FX views remain unchanged. We expect further

Dollar appreciation against most of the G10, driven by rising US rates

and reflecting the outperformance of US fundamentals. We forecast USD

strength to be most pronounced against the EUR, JPY and the commodity

currencies. Beyond the USD, we expect the GBP to be stronger vs the EUR

and commodity currencies," GS projects.