From Credit Agricole

The USD continues to ride the momentum in bonds yields, but there has been an important shift in the underlying driver of the yield curve.

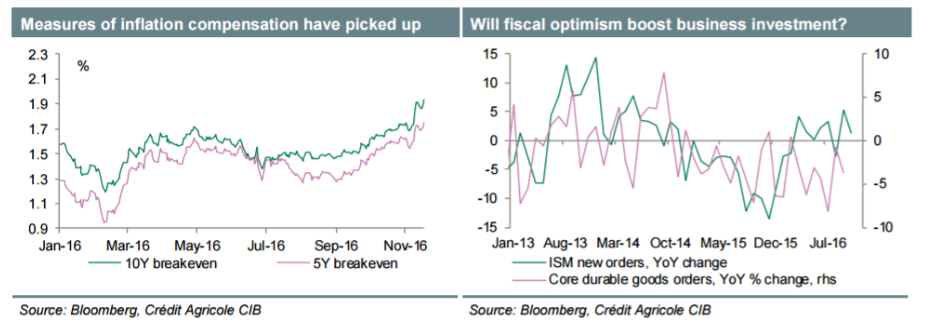

President-elect Trump has proposed an ambitious fiscal stimulus agenda, including USD1trn in infrastructure spending, cuts in personal and corporate taxes, and incentives to bring back corporate earnings retained abroad. While this agenda is likely to be significantly restrained by the fiscal hawks in Congress, even a moderate fiscal stimulus with an economy near full employment could generate inflationary pressures. These expectations are increasingly reflected in the US 10Y breakevens that are up some 20bp since the election. The tightening in financial conditions via higher bond yields should be of some concern for the Fed but in our view it will not deter the FOMC from hiking in December, especially as the move is more than 90% priced in. The Fed is likely to stick to its game plan of only very gradual rate increases thereafter as the fiscal outlook remains unclear for now. The USD may thus be reliant on the details of President Trump's cabinet, fiscal signals from recently re-nominated House Speaker Paul Ryan's and incoming inflation data to continue its uptrend.'

This week is shortened by the Thanksgiving holiday and probably does not lend itself to fresh USD highs but we suspect markets will continue buying into any corrective USD weakness.

On the economic calendar next week are October durable goods orders and the minutes from the November FOMC meeting, which should highlight that the Fed was in a wait-and-see mode ahead of the elections.

For bank trade ideas, check out eFX Plus.