The Reserve Bank of Australia decision is due at 0430GMT (5 April 2016) - here's a trading preview via eFX

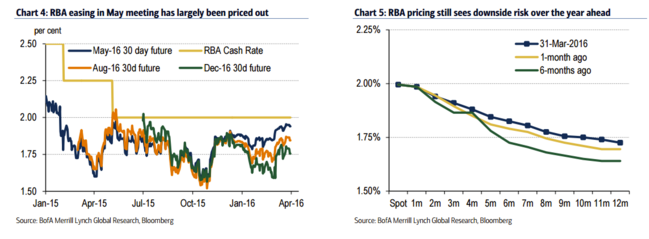

BofAML: Mounting Pressure On RBA; AUD More Than 7% Overvalued On RBA ModelThe RBA board meets on Tuesday 5th April. We expect the RBA to remain on hold at this meeting and for the rest of 2016. However, Governor Stevens' adherence to the benefits of maintaining a steady policy stance is coming under increasing pressure from factors largely out of his control as he runs down the clock on the last 6 months of his tenure. The Bank has been more open to acknowledging downside risks in China in recent months, but there is growing risk that the Bank's relatively upbeat forecasts on growth might come under more pressure from the unwelcome appreciation of the AUD. We estimate the AUD to be more than 7% overvalued based on the RBA's own equilibrium model.The dovish stance from the Fed adds another challenge to policy management on top of the extended move into negative rates territory in Europe and Japan. The current RBA cash rate of 2.0% looks increasingly attractive for investors on a relative basis. The AUD has gained almost 13% from January lows against the USD or nearly 8% on a TWI basis. The current TWI level of 64.2 is 3.5% above the level assumed in the economic forecasts presented in the February Statement on Monetary Policy (SMP). The Bank will have the next quarterly inflation data (due 27th April) and will update forecasts at the board meeting scheduled for 3rd May

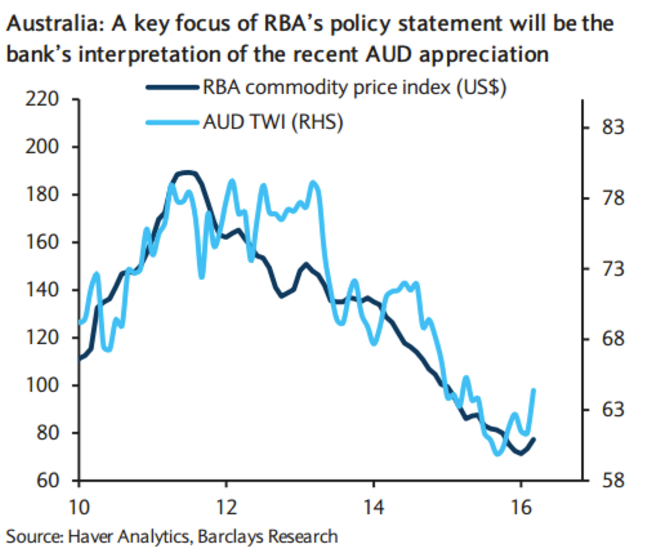

So far, RBA officials have used mild language to address the issue. Stevens suggested that the AUD rise "may be getting a bit ahead of itself" a week ago while other officials have expressed a preference for a "slightly lower" AUD. As such there is likely to be more focus on whether the Bank will amend the current line on the AUD: "The exchange rate has been adjusting to the evolving economic outlook." The risk is for some stronger language on the currency or in terms of the easing bias. Barclays: key focus is the rhetoric on AUD; Staying Long AUD/NZDThe RBA meets on Tuesday, and we and consensus expect it to stand pat in April. Q1 GDP has come in at a solid 0.6 q/q, and there has been no significant deterioration in domestic data since the March meeting. However, the trade-weighted AUD has appreciated near 5% since end-February, and commodity prices have also rallied sharply (Figure 8).As such, the key focus of this meeting is whether the RBA will resume "talking down" its currency by making adjustments to the discussion on the exchange rate in the statement.Considering that the AUD has moved alongside a rebound in commodity prices - implying that exchange rate valuation based on the RBA model may not have becom e overly misaligned even a fter the recent moves - and heightened attention on the RBA's rhetoric following the US Treasury's criticism of bank's "jawboning," we do not think that RBA will make significant adjustments to the statement on the excha nge rate this time. With soft wage growth and low inflation, we think the RBA will likely retain an easing bias, reiterating that "continued low inflation would provide scope for easier policy, should that be appropriate." Unless the RBA expresses a strong discomfort with the AUD rebound or tones down its easing bias, we see the RBA meeting as neutral for the AUDUSD.We continue, however, to recommend staying long AUDNZD,considering that the continued softening of consumer and business confidence in New Zealand as indicated by recent sentiment surveys suggests that the RBNZ is likely to be more uneasy about currency strength than the RBA.

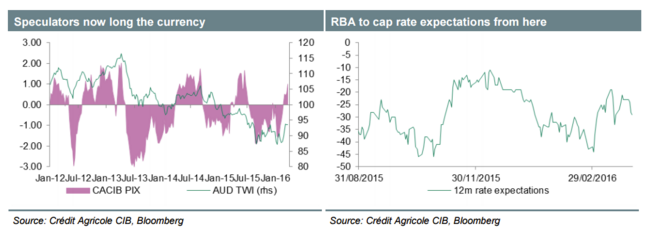

RBS: RBA on hold; no major changes in policy or language The RBA holds its April policy meeting tomorrow andwe match the consensus expecting no change in interest rates.The next decision, in early May, is due alongside the latest Statement on Monetary Policy, which includes updated growth and inflation forecasts. The RBA will also receive updated CPI inflation figures for the first quarter in mid-April, and the 2016 Federal Budget is due to be presented on May 3rd - the day of the May decision. With these major events upcoming in late April / early May,any major changes in policy or language may be unlikely this month.But we see a risk that the RBA signals that the inflation profile, which already (in the words of the RBA) would provide scope for easier policy, may be subject to new downside risks if the currency's strength is sustained. BNPP: RBA on Hold; Staying Short Vs NZD In Spot & Vs EUR In OptionsThe RBA holds a policy meeting tomorrow and while they have not taken recent opportunities to talk down the AUD, we think the risks are skewed towards the easing bias being made more explicit which would likely prompt the market to bring forward rate cut expectations (a full cut is priced only by the November meeting). We continue to see the AUD as overvalued on our short- and medium-term valuation metrics (STEER and CLEER) andremain short AUDNZD* via spot (targeting 1.0600) and long EURAUD via a call fly (expiry 16-Jun-16). Credit Agricole: Caution Warranted; AUD Positioning Near Overbought Territory The AUD has been among the strongest G10 FX currencies during the last few weeks. This was mainly due to a combination of better risk sentiment, stabilising commodity prices and improving growth conditions. Looking ahead, investors' focus turns to this week's RBA monetary policy announcement. In line with market expectations we see little scope of the central bank announcing additional policy measures at this meeting.However, it cannot be excluded that central bank Governor Steven will sound more cautious on the currency. Not long ago he stressed that the AUD may be getting ahead of itself. Considering that the currency has been appreciating further of late a more aggressive rhetoric may be required, especially when considering that growth momentum has failed to improve of late. As a result of the above outlined conditions caution is warranted. This is especially true as speculative positioning is close to overbought territory.